5 Myths About MEV: Separating Fiction from Reality in Decentralized Finance

Understanding MEV: Myths, Reality, and Protection Strategies

Maximal Extractable Value (MEV) has become one of the most misunderstood concepts in Decentralized Finance (DeFi). Some people always associate MEV with attacks, calling it an "MEV attack," while others claim that MEV itself is illegal. But is that really the case?

For example:

If traders equalize price discrepancies between Uniswap and Binance, is that an attack or an essential market function?

If loan positions in a lending protocol are updated after an Oracle transaction publishes new crypto prices, is that manipulation?

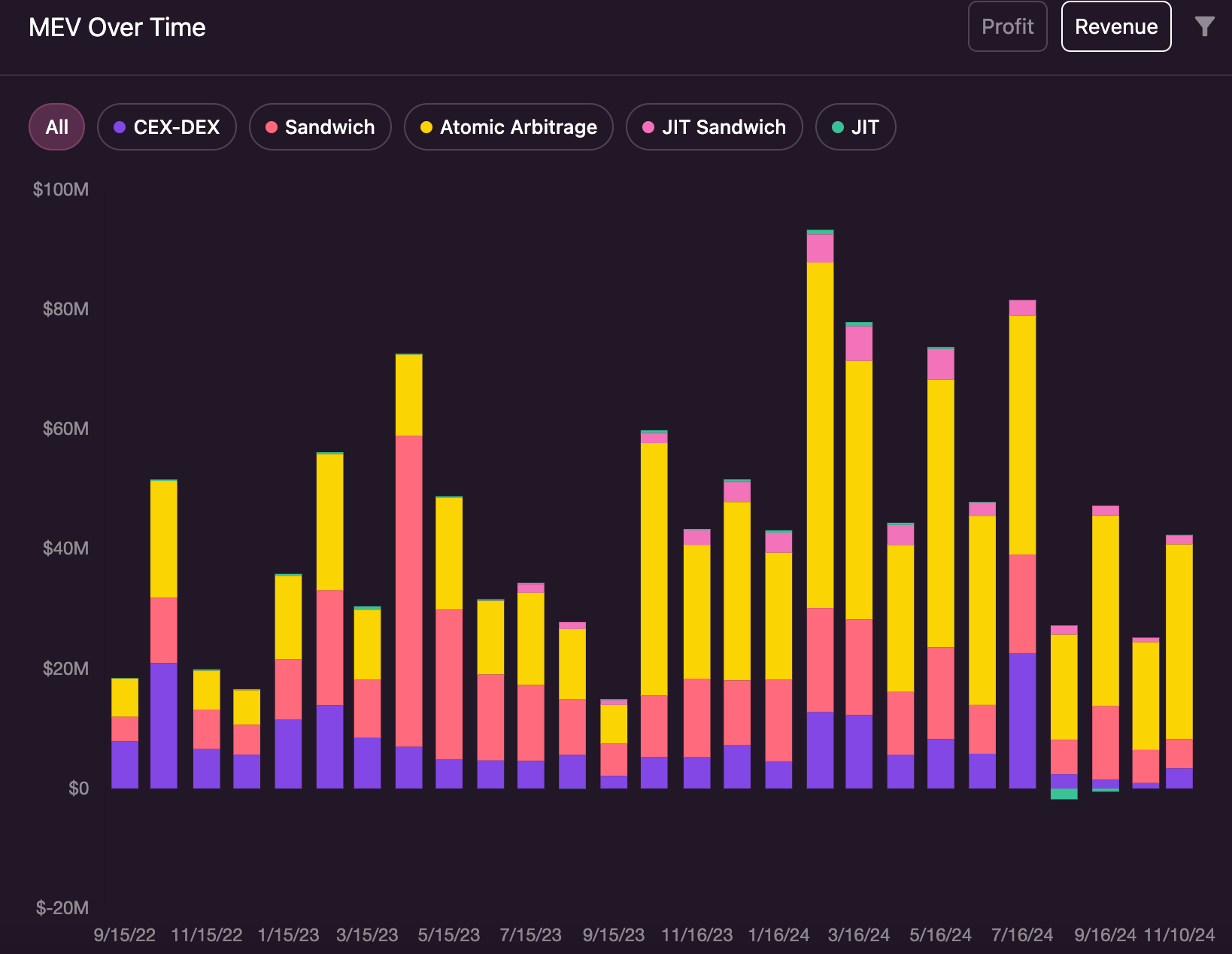

While certain types of MEV can be exploitative—such as front-running and sandwich attacks—these represent only about 10-15% of MEV cases. The majority of MEV consists of:

✅ 60% Arbitrage – Keeping DeFi markets efficient by aligning prices across exchanges.

✅ 30% Oracle Extractable Value – Updating lending protocols based on accurate, real-time pricing.

Moreover, many MEV attacks are not possible on Layer-2 (L2) blockchains like Arbitrum, Base, or ZKsync, where fair transaction ordering and sequencing reduce risk.

So, is MEV good or bad? And more importantly, how can we mitigate harmful MEV?

Background: What is MEV?

MEV refers to the reordering (or influencing the order) of transactions within a block to extract additional value. Validators or block producers decide the order of transactions, and in some cases, specialized MEV searchers find the opportunies to maximize profits by influencing this order.

On Ethereum, tools like MEV-Boost help manage MEV, while in some ecosystems, transaction ordering is entirely determined by block producers.

Types of MEV

1️⃣ Front-running – Placing a transaction before a target transaction to profit from its execution.

2️⃣ Back-running – Placing a transaction immediately after a target transaction to extract value.

3️⃣ Sandwich Attacks – A combination of front-running and back-running to manipulate asset prices.

Key MEV Concepts Explained

1. Oracle Extractable Value (OEV) & Liquidations

Oracles bring off-chain price data onto blockchains—for example, publishing the latest ETH/USDC exchange rate. When this data updates, it affects lending protocols that use the oracle to check loan health.

If a borrower’s position becomes undercollateralized, liquidation is triggered. MEV searchers race to liquidate bad loans and claim a liquidation bonus. This type of MEV is beneficial, as it ensures lending protocols remain solvent. It is a form of back-running MEV, in which liquidators back-run the oracle transaction.

2. Arbitrage MEV

Arbitrage traders help balance prices between exchanges. Since crypto assets trade on centralized exchanges (CEXs) like Binance and decentralized exchanges (DEXs) like Uniswap or Curve, price differences can emerge.

MEV searchers exploit these differences, ensuring prices remain aligned. Depending on where the arbitrage occurs, it falls into different categories:

🔄 DEX-DEX Arbitrage (Atomic) – Trades executed within a single transaction on-chain.

🔄 CEX-DEX Arbitrage (Non-Atomic) – Requires two separate trades, introducing execution risks.

🔄 Triangular Arbitrage (Atomic) – Exploiting pricing inefficiencies across three different trading pairs on-chain.

Arbitrage keeps DeFi markets efficient by ensuring price parity across platforms. It is also a form of the back-running MEV, in which arbitragers target the swap transactions that cause price disparities.

MEV "Attacks" Explained

While some MEV strategies are neutral or beneficial, certain forms of MEV are considered exploitative:

1. Sandwich Attacks

A trader detects a large swap order, places their own buy order before it, and sells immediately after, profiting from price impact.

✅ How to prevent it? Use MEV protection tools or trade in smaller amounts.

2. Just-in-Time (JIT) Liquidity Attacks

A liquidity provider detects a large swap, deposits liquidity just before the trade, earns a fee, and immediately withdraws.

✅ Impact? This benefits traders but comes at the expense of LPs, who lose trading fees.

The MEV Trilemma:

Is Any Blockchain MEV-Free?

No blockchain is entirely free from MEV. However, some chains have lower MEV activity due to lower user adoption or liquidity. The more valuable a chain’s transactions, the more opportunities arise for MEV extraction.

MEV on Layer 2 (L2) Blockchains

L2s like Arbitrum, Base, and zkSync significantly reduce MEV risks due to their different transaction ordering mechanisms.

L2s have no mempool (unlike Ethereum), making classic front-running attacks nearly impossible.

Sequencers control transaction order, making MEV harder to extract.

However, MEV still exists in L2s, especially in the form of arbitrage and oracle-based liquidations.

How to Protect Against MEV?

Ethereum

✅ MEV-Boost & Private Transaction Pools – Using private relays reduces exposure to public MEV searchers.

✅ MEV Protection Services – Some solutions, such as Flashbots, offer protection from sandwich attacks.

L2s

✅ Transaction Sequencing Models – L2s prevent classic front-running by controlling transaction order (as, they operate today on centralized sequencers).

✅ Solvers & Protected Execution – Aggregators and DEXs integrate solvers to prevent harmful MEV on swaps.

For retail users, MEV is rarely a concern, as MEV searchers mainly target large transactions where opportunities are higher.

New Trend: MEV Tax

While MEV is essential for DeFi efficiency, it often negatively impacts specific groups—especially liquidity providers (LPs).

For example:

LPs experience increased impermanent loss due to arbitrage-driven rebalancing.

MEV rewards are captured by validators or sequencers rather than returning to the DeFi ecosystem.

A new concept called MEV Tax proposes redistributing MEV revenue back to applications like Uniswap or lending protocols. These funds could then be distributed to:

✅ Liquidity providers (LPs)

✅ Traders & users

✅ Validators & facilitators

This aligns incentives, ensuring MEV benefits not just searchers and validators, but also DeFi participants. You can read more about it in this [research blog] by Paradigm.

5 Myths About MEV

Here are the five common misconceptions about MEV that many people misunderstand:

1️⃣ Myth: MEV is always an attack

Reality: Not all MEV is harmful. While front-running and sandwich attacks can be exploitative, most MEV (~90%) is actually neutral or beneficial:

✅ 60% Arbitrage – Equalizing prices across DEXs and CEXs.

✅ 30% Oracle-Based Liquidations – Keeping lending protocols solvent.

Only ~10-15% of MEV consists of malicious attacks like sandwich trading.

2️⃣ Myth: MEV is illegal

Reality: MEV is not illegal, and in fact, it serves an important role in market efficiency.

Arbitrage keeps prices fair across markets.

Liquidations ensure lending protocols remain solvent.

Validators and sequencers legally reorder transactions based on incentives.

However, some forms of MEV (e.g., front-running users with private information) may raise ethical and regulatory concerns.

3️⃣ Myth: MEV is only a problem on Ethereum

Reality: MEV exists on every blockchain where transaction order can be manipulated.

Ethereum and other Layer-1 chains have public mempools, making them highly exposed to MEV.

L2s like Arbitrum, Base, and zkSync significantly reduce certain types of MEV, but arbitrage and liquidation-based MEV still exist.

Even Solana, Avalanche, and Cosmos face MEV challenges through validator-controlled ordering.

MEV is a fundamental issue across all decentralized networks, but its impact varies by architecture.

4️⃣ Myth: MEV only affects traders

Reality: MEV impacts many different participants in DeFi:

Traders – Can suffer sandwich attacks, leading to higher slippage and worse prices.

Liquidity Providers (LPs) – Face impermanent loss due to arbitrage-driven rebalancing.

Validators & Sequencers – Earn MEV rewards from transaction ordering.

Lending Protocol Users – May have their positions liquidated faster due to oracle-based MEV.

MEV redistributes value within DeFi. Some benefit, some lose—it depends on your role in the ecosystem.

5️⃣ Myth: MEV can be completely eliminated

Reality: MEV cannot be fully removed, but it can be mitigated:

✅ MEV-Boost & Private Relays – Reduce harmful front-running.

✅ Fair Sequencing on L2s – Controls transaction ordering to prevent unfair MEV extraction.

✅ MEV Taxation & Redistribution – Ensures MEV benefits LPs & users instead of just validators.

While some projects aim to minimize MEV, it is an inevitable feature of blockchain transaction ordering. Instead of eliminating it, the goal is to make MEV fairer and more transparent.

Conclusion:

The Future of MEV in DeFi

MEV is often misunderstood as purely harmful, but in reality, it is a complex phenomenon that plays a key role in DeFi markets. Some forms of MEV are necessary for price efficiency and protocol security, while others can be harmful to users and liquidity providers.

MEV is not inherently bad—it plays a critical role in market efficiency, ensuring fair prices and liquid markets. However, some forms of MEV negatively impact LPs and traders, which is why new protection mechanisms and MEV redistribution strategies are emerging.

Key Takeaways:

✅ Most MEV is neutral or beneficial – 60% is arbitrage, 30% is oracle-based liquidations.

✅ MEV risks vary by blockchain – L2s reduce classic MEV risks, but arbitrage and OEV remain.

✅ Protections are improving – MEV-Boost, private relays, and L2 sequencing models help mitigate risks.

✅ MEV Tax could reshape incentives – Redistributing MEV revenue to LPs and traders aligns DeFi with fairer value capture.

With MEV protection tools, Layer-2 solutions, and fairer MEV redistribution models, we are entering an era where MEV can be better controlled and more equitably distributed.

📩 Want to explore MEV protection strategies or better MEV management for your institution? Let’s connect and discuss how DeFi can evolve for a fairer future.