5 Reasons why Deutsche Bank went for Layer-2 Blockchain

Exploring the Drivers, Benefits, and Challenges of Layer-2 Adoption in Finance

Just before the Christmas break, Deutsche Bank, a leading European financial institution, announced the launch of its new blockchain initiative, leveraging a layer-2 blockchain solution. While many banks, such as JP Morgan, have experimented with blockchain technology, Deutsche Bank's announcement stands out because it marks the bank's first foray into layer-2 blockchains. This move signals a strategic shift in how financial institutions view scalability, security, and privacy in blockchain technology. But what are the drivers behind this decision? And how do layer-2 solutions compare to layer-1 blockchains?

Understanding Layer-1 vs. Layer-2 Blockchains

To grasp the significance of Deutsche Bank's decision, it is essential to understand the difference between layer-1 and layer-2 blockchains.

Layer-1 Blockchains

Layer-1 blockchains, such as Bitcoin, Ethereum, or Hyperledger, operate their own physical network of nodes (validators or miners) to achieve consensus on the state of the ledger. While secure and decentralized, these networks often struggle with scalability and high transaction fees.

Layer-2 Blockchains

Layer-2 blockchains offer a different approach to scaling by building on top of existing layer-1 networks. Instead of creating a new network of nodes and a new consensus mechanism, layer-2 solutions inherit the security and decentralization properties of the underlying layer-1 blockchain. This makes them more scalable and cost-efficient compared to launching entirely new blockchains.

There are various types of layer-2 scaling solutions, including:

Payment Channels (e.g., Bitcoin's Lightning Network): Facilitate fast, low-cost payments.

Plasma Chains: Use side chains to bundle transactions.

Rollups: The most prominent type of layer-2 solution, particularly relevant for institutional use cases.

What Are Rollups and How Do They Work?

Rollups are a type of layer-2 blockchain that processes transactions off-chain and then posts transaction data to the underlying layer-1 blockchain (such as Ethereum). This approach significantly reduces gas fees and increases throughput without compromising security.

How Rollups Operate

Rollups are typically managed by a centralized operator known as a sequencer, responsible for bundling (or "rolling up") transactions into batches and submitting them to the layer-1 blockchain. Depending on the validation mechanism, rollups can be categorized into two types:

Optimistic Rollups

Assume that transactions are valid by default.

Introduce a challenge period (typically seven days) during which anyone can dispute the validity of a transaction.

Fully compatible with the Ethereum Virtual Machine (EVM), enabling seamless deployment of existing Ethereum smart contracts.

Zero-Knowledge (ZK) Rollups

Use cryptographic proofs (zero-knowledge proofs) to verify transactions.

Faster finality compared to optimistic rollups, with transaction settlement within hours or even minutes.

More expensive to operate due to the computational cost of generating zero-knowledge proofs.

Optimistic vs. ZK Rollups: Pros and Cons

Both types of rollups have their advantages and disadvantages:

Feature Optimistic Rollups ZK Rollups EVM Compatibility Full Partial or None Finality Time Up to 1 week 1 hour to 1 day Transaction Costs Lower upfront Higher due to ZK proof generation Data Privacy Less privacy (must post transaction details) Greater privacy (proofs without full details)

For financial institutions, ZK rollups offer a particularly compelling feature: enhanced privacy. Unlike optimistic rollups, ZK rollups do not need to post all transaction details to the underlying layer-1 blockchain. This can be crucial for compliance with privacy regulations in financial transactions.

Deutsche Bank implemented a permissioned ZK rollup on Ethereum.

Blockchain in the Financial Industry

Financial institutions have experimented with various blockchain architectures, including public, permissionless blockchains and permissioned blockchains. Let's compare these approaches:

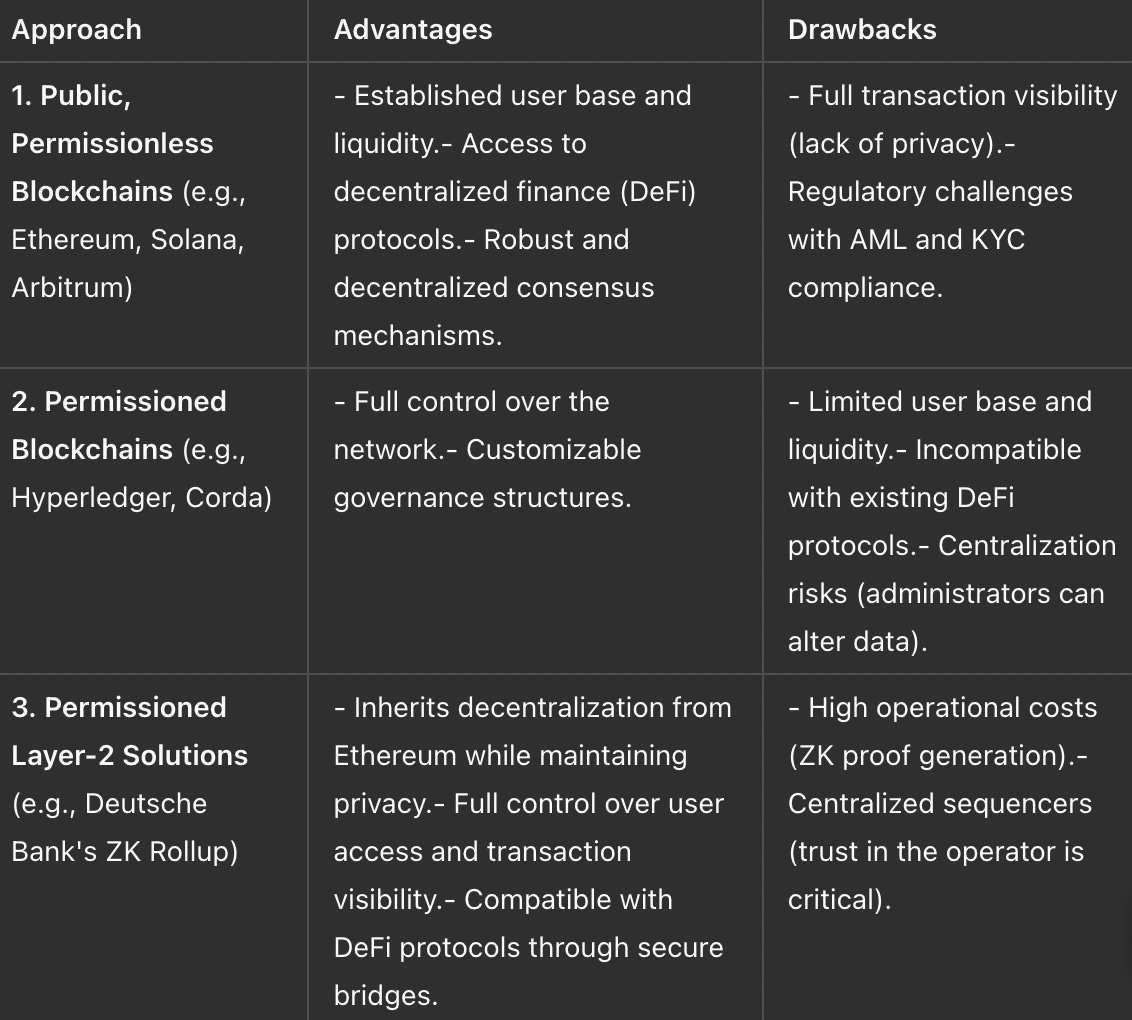

1. Public, Permissionless Blockchains (e.g., Ethereum, Solana, Arbitrum)

Advantages:

Established user base and liquidity.

Access to decentralized finance (DeFi) protocols.

Robust and decentralized consensus mechanisms.

Drawbacks:

Full transaction visibility (lack of privacy).

Regulatory challenges with AML and KYC compliance.

2. Permissioned Blockchains (e.g., Hyperledger, Corda)

Advantages:

Full control over the network.

Customizable governance structures.

Drawbacks:

Limited user base and liquidity.

Incompatible with existing DeFi protocols.

Centralization risks (administrators can alter data).

3. Permissioned Layer-2 Solutions (e.g., Deutsche Bank's ZK rollup)

Advantages:

Inherits decentralization from Ethereum while maintaining privacy.

Full control over user access and transaction visibility.

Compatible with DeFi protocols through secure bridges.

Drawbacks:

High operational costs (ZK proof generation).

Centralized sequencers (trust in the operator is critical).

Providers of Layer-2 Solutions

Several companies offer frameworks to deploy rollups, including:

Elastic Chain from zkSync/Matter Labs (zk rollups)

Orbit from Arbitrum/Offchain Labs (optimistic rollups)

Optimism's Superchain (optimistic rollups)

These providers are actively working on improving decentralization, interoperability, and scalability of layer-2 solutions.

Why Layer-2 for Financial Institutions?

Layer-2 blockchains are not a replacement for existing layer-1 networks; rather, they complement them. While layer-1 blockchains serve as secure stores of value for tokenized assets, layer-2 solutions provide:

Scalability: Faster transaction throughput and lower fees.

Privacy: Controlled visibility of transaction data.

DeFi Integration: Ability to run DeFi protocols and interact with public blockchains through secure bridges.

For financial institutions like Deutsche Bank, adopting layer-2 solutions can unlock new opportunities in tokenized assets, cross-border payments, and decentralized finance, all while maintaining compliance with regulatory requirements.

Conclusion

Here are five key reasons why Deutsche Bank's move to a layer-2 blockchain is significant:

1. Scalability and Cost Efficiency

Layer-2 solutions like rollups dramatically reduce transaction costs and increase throughput. For financial institutions, this means they can process a higher volume of transactions without the prohibitive gas fees associated with layer-1 blockchains like Ethereum. Unlike permissioned layer-1 chains, L2s do not require heavy infrastructure investments to achieve decentralization and avoid centralization risks.

Traditional banking systems handle millions of transactions daily. Layer-2 scalability is critical to bringing blockchain into mainstream finance.

2. Enhanced Privacy for Financial Transactions

Zero-Knowledge (ZK) rollups, which Deutsche Bank is reportedly adopting, provide greater privacy by not requiring all transaction details to be posted on the underlying layer-1 chain. This privacy feature is particularly valuable for financial institutions that need to comply with strict confidentiality regulations.

Privacy is a top priority in financial services. ZK rollups can ensure compliance with data protection laws while maintaining transparency where necessary.

3. Compatibility with Existing DeFi Protocols

Layer-2 solutions are often compatible with the Ethereum Virtual Machine (EVM), allowing financial institutions to leverage existing DeFi infrastructure like lending protocols, tokenized assets, and automated market makers (AMMs). This compatibility reduces development costs and accelerates adoption.

Deutsche Bank can tap into the existing DeFi ecosystem without building everything from scratch, speeding up their blockchain adoption journey.

4. Lower Regulatory Risks

By using layer-2 solutions, financial institutions can retain control over who has access to transaction data, making it easier to comply with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. Permissioned layer-2 blockchains allow institutions to manage participants while still benefiting from Ethereum’s decentralized infrastructure.

Compliance is a major concern for banks. Layer-2 can offer a balance between decentralization and regulatory control.

5. Future-Proofing with Interoperability

Layer-2 blockchains are designed to interact seamlessly with layer-1 chains like Ethereum. This interoperability ensures that Deutsche Bank’s blockchain infrastructure will remain relevant as the broader DeFi ecosystem evolves.

The blockchain space is constantly evolving. Deutsche Bank’s choice of a layer-2 solution keeps them adaptable and positioned for long-term success.

Deutsche Bank's decision to launch a layer-2 blockchain marks a pivotal moment for institutional adoption of decentralized finance. By leveraging the scalability and privacy features of rollups, financial institutions can balance the need for innovation with the requirements of security and compliance. As the ecosystem evolves, layer-2 solutions are likely to become integral to the future of finance, bridging the gap between traditional banking and decentralized finance.