7 System-Level Security Risks in Institutional DeFi: From Order Flow to Governance

Risk does not sit inside one smart contract. It emerges from cross-layer interaction, incentive design, order flow power, and governance control.

Every week we hear about another institution entering DeFi: a new asset manager launching an on-chain strategy, a stablecoin issuer expanding into new markets, or an RWA platform bringing new forms of collateral on-chain.

The scale of capital being discussed is materially different from early DeFi cycles. It is larger, more structured, and measured in tens or hundreds of millions. However, the risk discussion often remains narrow. These are not “smart contract hack” scenarios, but structural risks embedded in the architecture you rely on.

Institutional DeFi exposure spans multiple interacting layers - regardless of whether the base layer is Ethereum, Solana, or another blockchain. The same structural dependencies exist:

Base Layer (L1): consensus, finality, and data availability

Execution Layers (L2s or appchains): high-throughput environments, often with privileged sequencing actors that determine order flow

DeFi protocols: DEX, lending markets, vaults, derivatives platforms

Bridges and cross-chain routers: asset transfers and message passing between domains

Oracles: external data feeds used for pricing, collateral valuation, and liquidations

Governance systems: multisigs, upgrade keys, parameter control, emergency functions

Allocating capital into DeFi means relying on the integrity, coordination, and economic stability of all these layers simultaneously. Risk does not sit inside one smart contract.

It emerges from cross-layer interaction, incentive design, order flow power, and governance control.

The rest of this article breaks down the major system-level risks institutional capital must explicitly model before scaling on-chain exposure.

1. Settlement Layer Risk (Base-Layer Dependence)

Whether you deploy on Ethereum, Solana, or another public blockchain, institutional exposure ultimately depends on the properties of the base settlement layer. Rollups (L2 blockchains) inherit security and finality from an underlying consensus system. Institutional exposure, therefore depends on:

Honest-majority consensus assumptions

Deterministic finality guarantees (when your transaction becomes irreversible from the blockchain ledger)

Network congestion behavior

Fee market dynamics under stress

If the base layer becomes congested or unstable, cross-layer settlement slows down. Exit paths become delayed. Forced liquidations may executed at unfavorable times.

History provides clear examples. During periods of extreme NFT minting activity, gas fees on Ethereum spiked to thousands of dollars per transaction. In 2022, the Yuga Labs Otherside mint led to severe congestion and transaction failures across the network. On Solana, extremely high transaction numbers caused the blockchain to halt its functioning entirely for even 6 hours!

For retail participants this is inconvenient.

For institutions, this becomes a redemption timing and liquidity risk.

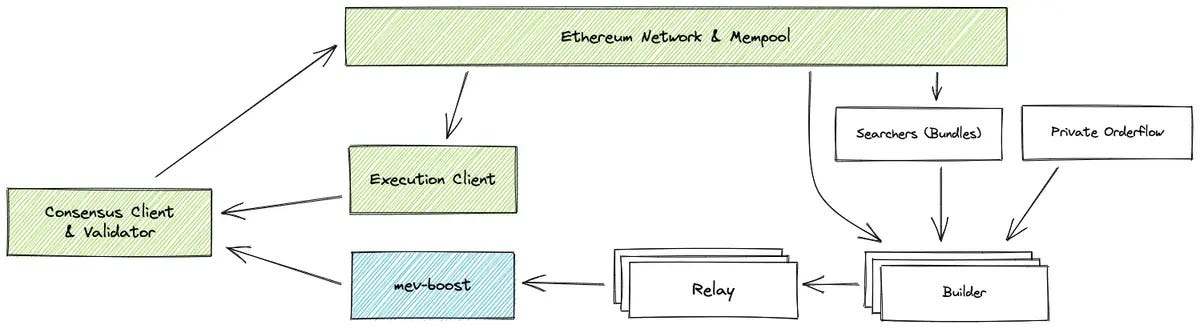

2. Order Flow and MEV (Execution Asymmetry)

Blockchains do not guarantee neutral execution. Whether on Ethereum, Solana, or private networks, transactions typically pass through a mempool before being included in a block.

A mempool is a waiting area for pending transactions. On networks like Ethereum, this pool is visible to everyone. This creates transparency, but also strategic vulnerability. Large trades, liquidations, or redemptions can be anticipated and economically exploited before confirmation. For institutional-sized transactions, this becomes material.

If a transaction is visible before execution, it can be:

Copied

Reordered

Sandwiched

Backrun

Used as input for arbitrage

This is the foundation of what is commonly referred to as MEV (Maximal Extractable Value).

Ethereum has evolved toward architectures such as proposer-builder separation (PBS), where block construction and block proposal are separated. This improves specialization and market efficiency.

This setup allows transactions to be submitted through private relay systems rather than the public mempool. These systems forward transactions directly to block builders. In this model:

The transaction is not publicly visible before execution

It becomes visible only once included in a block

For institutions, private submission is often a minimum requirement for large trades.

Some forms of arbitrage and liquidation are necessary for DeFi to function efficiently. They maintain price alignment and solvency. The existence of MEV is not inherently problematic. The risk arises when execution asymmetry is unmodeled, unpriced, or misunderstood.

This is not a “hack” scenario.

It is a structural execution risk embedded in how transactions are observed, ordered, and finalized.

3. Liquidity Fragmentation Risk

Liquidity in DeFi is not unified. It is fragmented across L1, multiple L2s, application-specific chains or isolated lending pools and vaults For institutions, this fragmentation creates three structural problems:

Capital inefficiency – Liquidity must be deployed across multiple venues to access opportunity.

Slippage under size – Large trades move markets, especially in fragmented pools.

Yield compression – In lending markets and vaults, APY is directly dependent on utilization. The more capital you deploy, the lower your marginal yield.

Most yield dashboards and aggregators do not model capital impact. They show static APY, not marginal APY under institutional size.

On the trading side, slippage and MEV risks increase with order size. Solver-based execution systems such as CoW-style batch auctions or intent-based routing can mitigate some of this, but fragmentation remains structural.

During stress events, liquidity can evaporate quickly. Institutions discover that quoted liquidity and executable liquidity are not the same.

Fragmentation creates hidden opportunity cost and exit friction.

4. Oracle and Valuation Risk

Tokenized RWAs and lending markets rely on external price feeds.

Even robust oracle systems are exposed to:

Short-term manipulation within deviation thresholds

Latency between market moves and on-chain updates

Liquidity-dependent pricing distortions

In leveraged systems, small distortions can trigger:

Forced liquidations

Liquidation cascades

Stablecoin supply contraction

Oracle risk is rarely binary. It does not require full oracle failure.

It only requires temporary distortion within accepted parameters.

For institutions deploying leveraged or collateralized structures, this becomes a solvency modeling issue.

5. Governance and Upgrade Risk

Protocols evolve. Governance can:

Modify collateral factors

Adjust liquidation thresholds

Change interest-rate curves

Upgrade smart contracts

Pause critical functionality

From an institutional perspective, this represents embedded counterparty exposure.

Even if governance is non-malicious, parameter changes during stress can materially affect positions. Emergency pauses can lock liquidity. Upgrade risk introduces execution uncertainty.

Institutional allocation requires explicit modeling of who controls upgrade keys, how governance decisions are made, and what the response time is under crisis.

6. Cross-Domain Settlement and Bridge Risk

Tokenized RWAs and stablecoins increasingly operate across multiple domains:

L1 ↔ L2

L2 ↔ L2

Rollup ↔ appchain

On-chain ↔ off-chain systems

Each bridge introduces:

Proof verification assumptions

Message finalization delays

Data availability dependencies

Cross-domain settlement risk is frequently underestimated in institutional models.

Exit timing, redemption flows, and liquidity routing depend on bridge finality and liveness guarantees.

Institutions must ask:

What is the worst-case withdrawal time?

What happens under sequencer halt?

What if data availability is temporarily disrupted?

Bridge architecture is not just a technical concern. It is a capital mobility constraint.

7. Liquidity Shock and Forced Liquidation Spiral Risk

The most misunderstood risk is systemic liquidity spiral risk.

Under stress:

Prices decline

Liquidations trigger

Liquidity thins

Slippage increases

Additional liquidations trigger

On rollups, sequencing power and latency amplify this dynamic. Liquidations may cluster within short windows. Market depth may not absorb forced selling.

For RWA issuers and stablecoin systems, this can lead to:

Temporary depegs

Redemption bottlenecks

Yield collapse

Capital flight

This is not a protocol bug.

It is an equilibrium outcome under stressed liquidity and leverage conditions.

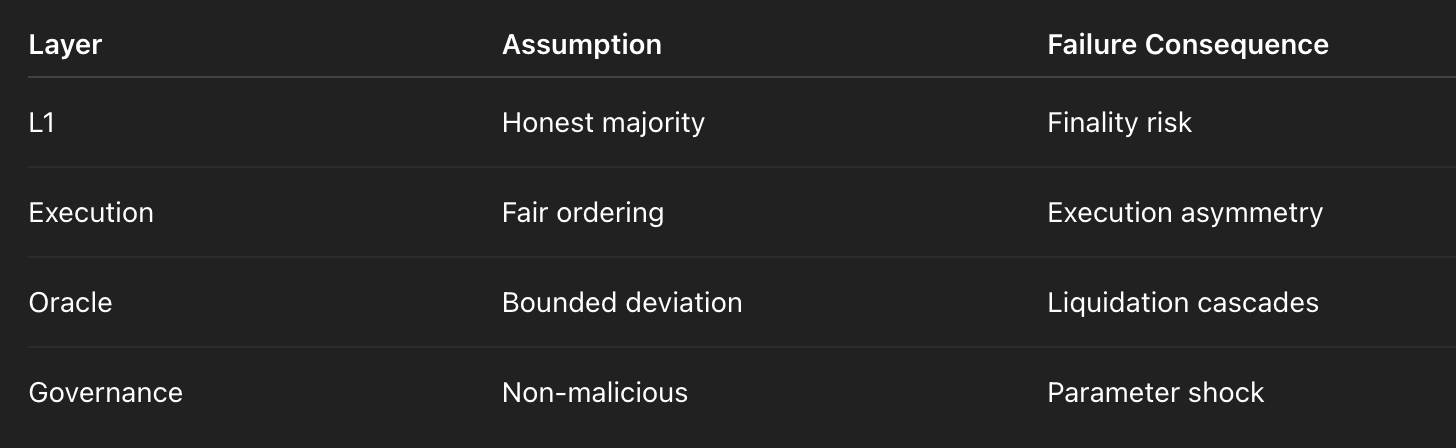

Explicit Trust Assumptions

Every institutional deployment implicitly assumes:

The base blockchain layer operates under honest-majority consensus

Transactions (from mempool) are ordered fairly for execution

Data availability mechanisms function within bounds

Governance keys are not malicious or compromised

Oracles remain within bounded manipulation thresholds

The issue is not that these assumptions exist.

The issue is when they are not written down and stress-tested.

Closing Thoughts

Institutional DeFi risk is not protocol-specific. It is architectural. The seven risk domains discussed above share a common feature: they emerge from the interaction of consensus, execution, liquidity, governance, and cross-domain settlement.

A protocol audit tests code.

A yield dashboard shows returns.

Neither models structural exposure.

An institutional-grade framework must explicitly document:

Settlement assumptions at the base blockchain layer

Order flow control

Liquidity depth under institutional size

Governance authority and upgrade rights

Cross-domain exit guarantees

Without this, exposure remains implicit. Institutions that formalize these assumptions deploy capital with structural clarity. The next phase of institutional DeFi will not be defined by innovation alone. It will be defined by better risk architecture.

If this framework is relevant to your DeFi allocation, RWA issuance, I am happy to discuss how to operationalize it.