Liquidity Fragmentation: Are LPs Rational or Just Losing Money? Part I

As more L2s emerge—such as Arbitrum, Base, zkSync, Optimism, or recently Unichain—liquidity providers (LPs) face a growing challenge: Where should they allocate their liqudity to maximize returns?

Just before spring break, I had the privilege of attending the Financial Cryptography and Data Security Conference (FC25)—widely regarded as one of the top academic venues for blockchain and security research. I spoke at the co-located Crypto Asset Analytic Workshop (CAAW25), sharing insights into a growing challenge in DeFi: liquidity fragmentation across Layer 2s.

As more L2s come online—Arbitrum, Base, zkSync, Optimism, and recently Unichain—liquidity providers (LPs) are facing a hard question: Where should I deposit my liquidity to maximize returns?

As more L2s emerge—such as Arbitrum, Base, zkSync, Optimism, or recently Unichain—liquidity providers (LPs) face a growing challenge: Where should they allocate their liqudity to maximize returns? While traders have already migrated to L2s for faster and cheaper transactions, the optimal strategy for LPs remains less clear.

Why Providing Liquidity Isn’t Risk-Free

Liquidity provision in automated market makers (AMMs) like Uniswap offers LPs a share of the trading fees generated by swaps. However, this comes with a well-known risk: impermanent loss. Here is a simplified explanation:

AMMs set swap prices based on the ratio of tokens held in a liquidity pool.

As trades occur, this ratio shifts.

Consequently, LPs hold a greater share of the assets that have depreciated in value and less of the ones that have appreciated.

This leads to a loss relative to simply holding the assets, called impermanent loss.

The LP is profitable only if the trading fees collected exceed the impermanent loss.

Our Research:

Comparing LP Returns Across Chains

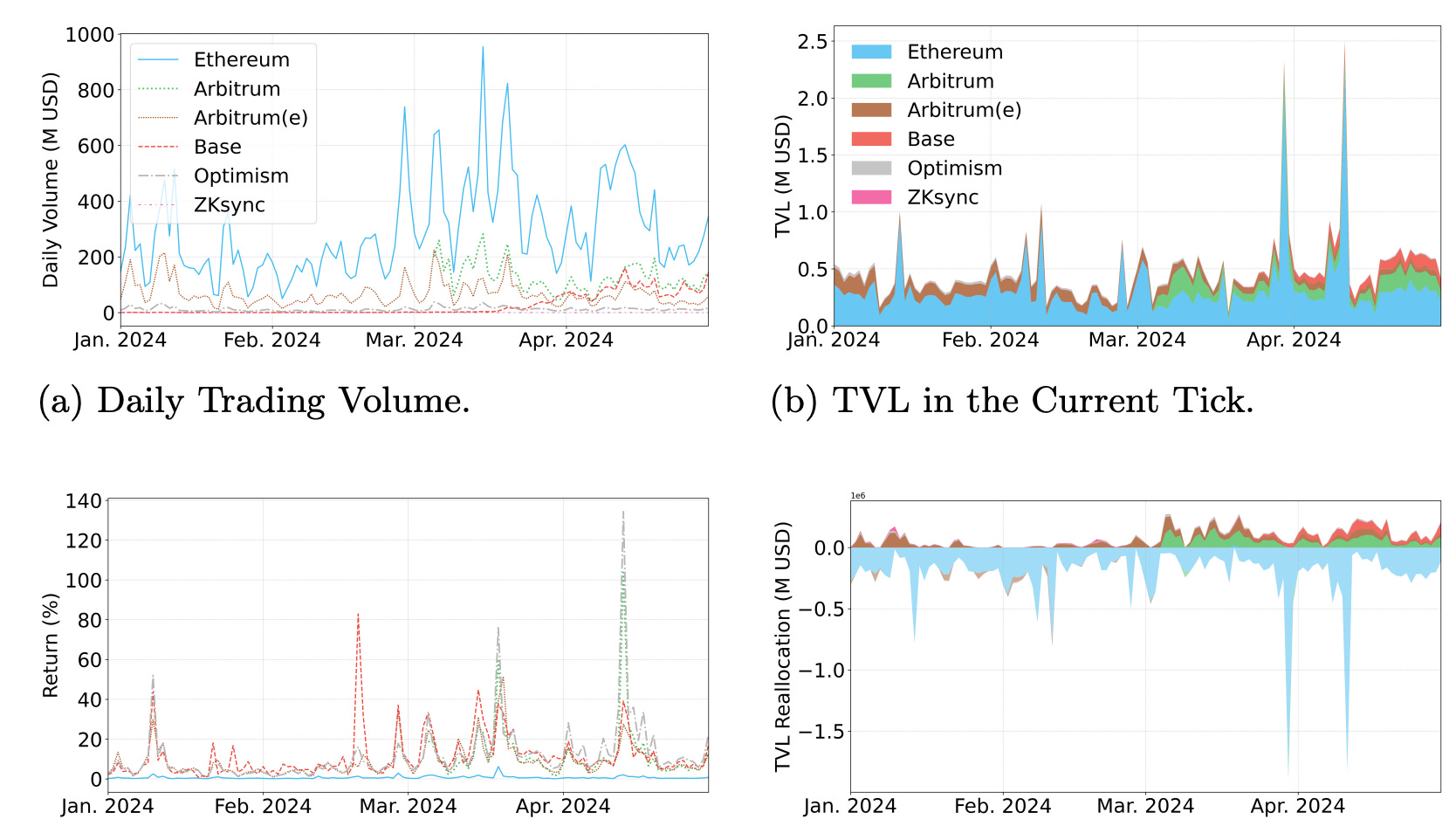

We set out to ask a different question: Given the same token pair (USDC-ETH), how do LPs behave across different chains?

We looked at Uniswap v3 pools on:

Ethereum (L1)

Arbitrum

Base

Optimism

zkSync

Because it’s the same USDC-ETH pool, impermanent loss is identical across chains. That isolates differences in LP behavior and rewards.

Key Finding: Overcapitalization on Ethereum

Our results show that Ethereum’s USDC-ETH pool is significantly overcapitalized.

In fact, LPs could have reallocated up to 60% of their capital to L2s and earned substantially higher net returns.

Why does this happen?

Ethereum still has the highest total trade volume.

However, fees are shared among all LPs in the pool on a pro-rata basis.

The high total value locked (TVL) on Ethereum dilutes returns for individual LPs.

In contrast, L2s—despite lower volume—offer more favorable fee-to-TVL ratios, resulting in higher effective yields for LPs.

In short, many LPs are not optimizing their capital allocation, potentially due to inertia, perceived security on L1, or lack of cross-chain tooling.

Theoretical Model of LP Optimization

We also present a formal model describing how rational LPs should distribute their capital across chains to optimize returns. The model accounts for:

Trading fees,

Impermanent loss,

TVL dilution, and

Operational costs such as gas fees and bridging delays.

According to the model, if all LPs behaved rationally, returns across chains would eventually converge toward an equilibrium rate. In this mature state, differences in returns would reflect only structural factors (e.g., base-layer risks or execution latencies), not inefficiencies in capital allocation.

Final Thoughts

Liquidity fragmentation is no longer a theoretical concern—it is a real and measurable inefficiency in the DeFi ecosystem. As the multichain landscape evolves, LPs who proactively optimize their strategies can capture meaningful excess returns. Conversely, those who continue to provide liquidity without considering cross-chain opportunities may underperform significantly.

You can access to full paper at: https://arxiv.org/pdf/2410.10324