Wintermute enters Morpho curation: the case for Select Vault, and the questions to ask

A look at Wintermute’s two new Armitage vaults on Morpho, with particular attention to the v-wmtUSDC / Wildcat integration inside the Select vault.

Wintermute, the market-making firm that has long been one of the most active DeFi liquidity providers, has now stepped onto the vault curator side of the stack. Through its Armitage brand it has launched two Morpho-curated USDC vaults: Prime and Select. Initial supply is roughly $50M across the two, with Prime currently at ~3–4.5% net APY and Select targeting 5–8%, currently around 6% once the new v-wmtUSDC market is fully allocated.

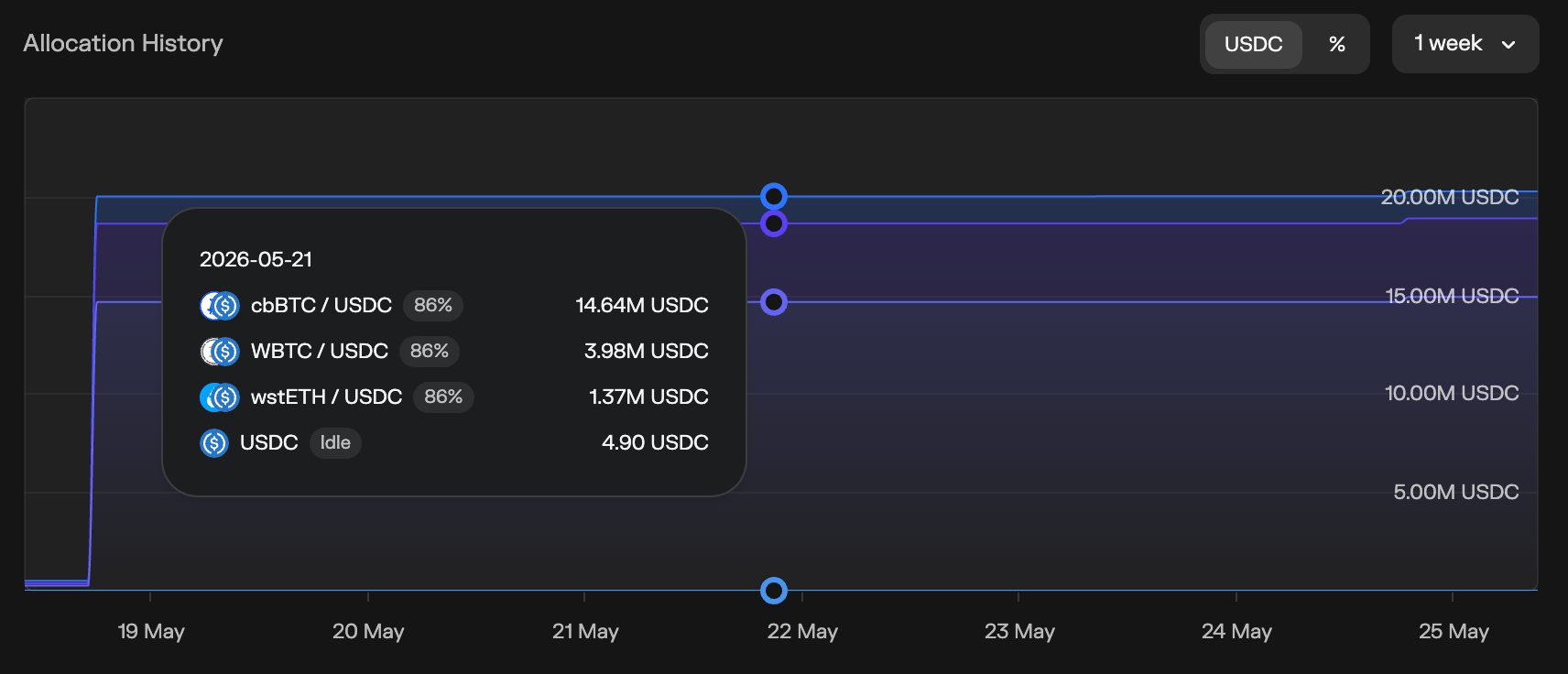

That last number is what makes the Select vault interesting. The yield premium comes from tokenized RWA, precisely a new collateral type Wintermute has onboarded into Morpho - a wrapped position in its own Wildcat credit market.

Background: what a Morpho vault is, and why RWA issuers want in

Morpho is a permissionless lending protocol with two new DeFi primitives. The first is isolated credit markets - each market pairs exactly one collateral asset with exactly one borrow asset (for example, wstETH / USDC), with its own loan-to-value (LTV), liquidation threshold and oracle. Bad debt in one market is contained inside that market. The second primitive is the vaults that sit on top: a vault accepts USDC deposits from passive lenders and re-allocates that USDC across whitelisted isolated markets according to a set of caps and parameters chosen by the curator.

Curators are the credit officers of DeFi. Gauntlet, Steakhouse, KPK, Galaxy and now Armitage (Wintermute) all sit in this role. The curator decides which collateral types enter the vault, what LTV is acceptable, which oracle is trusted, and how much capital can be deployed against any one collateral.

Tokenised RWAs reach DeFi through exactly this layer. The RWA token is admitted into an isolated market against USDC; the curator sets the parameters; the vault deposits flow into that market when a borrower needs leverage. For a tokenised credit token, this is the most efficient distribution channel into onchain capital - a holder can borrow USDC against the token, recycle the USDC into more of the token, and the issuer gets continuous demand-side flow without minimum-ticket or redemption-window friction.

The vault is also the natural risk container. If the RWA market breaks, the loss is bounded by the cap that the curator set, not socialised across all DeFi.

The two Armitage vaults: same architecture, different risk profiles

Prime is the conservative vault. The accepted collateral list is the standard blue-chip stack: wrapped BTC, wrapped ETH, liquid-staked ETH (wstETH, weETH). This is the same risk profile that Gauntlet, Steakhouse, Galaxy and KPK USDC vaults already offer, which is exactly why Prime yields a similar 3–4.5% - there is no structural reason for it to clear above the peers.

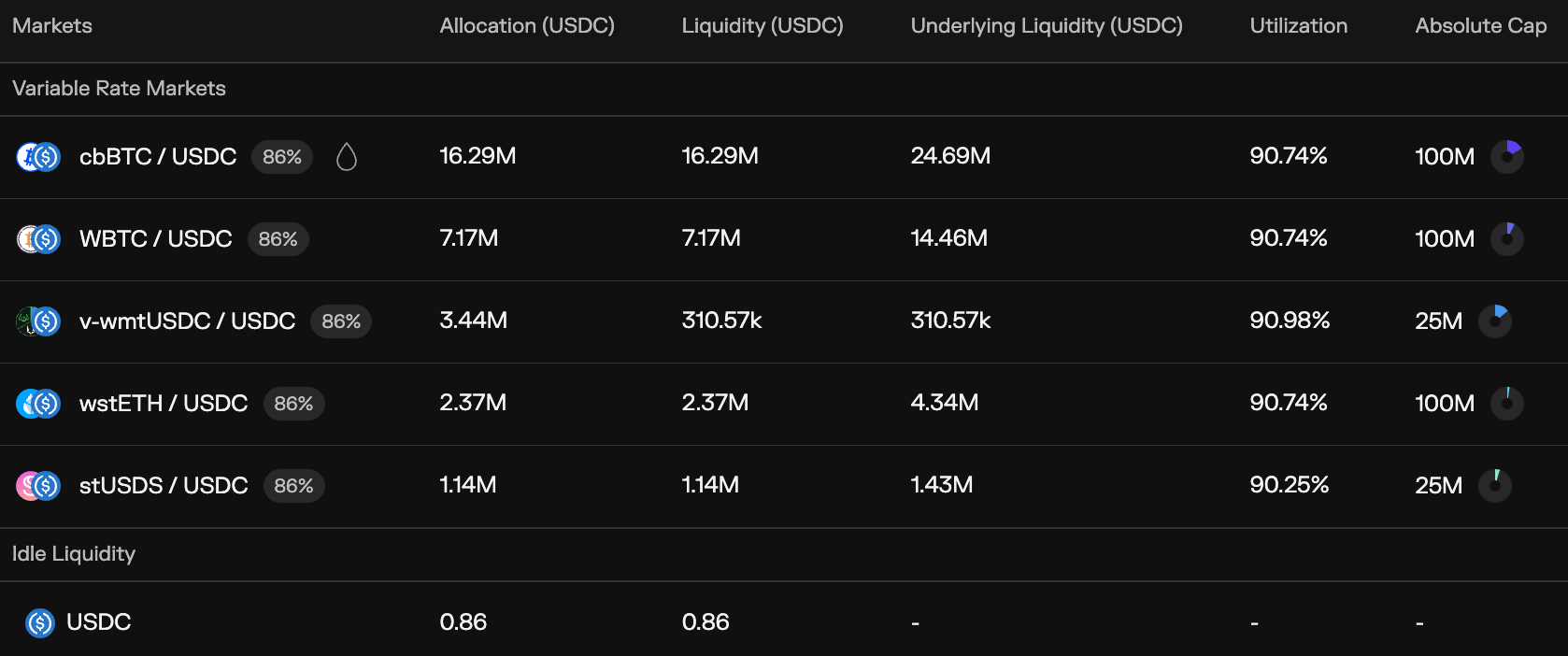

Select starts from the same blue-chip base but explicitly admits additional collateral classes that Prime does not: tokenized RWAs. The first non-blue-chip market Wintermute has onboarded into Select is v-wmtUSDC as collateral against USDC. This intention brings higher-yielding credit exposure into Morpho.

If Wintermute can keep onboarding well-priced credit exposure on the Select side at 6–8% net to the LP, this becomes one of the more interesting curator products on Morpho. If the credit underwriting is wrong, the same structure is what will produce the loss.

RWA in vaults: the four risks to watch

Independent of any specific issuer, the same four risks recur every time an RWA token is admitted as collateral into a vault:

Oracle / NAV. Where does the price come from, who publishes it, how often, what happens when it is stale. For a tokenized credit position, there is no organic on-chain price, so the curator has to choose between an independent-published (and calculated) NAV feed, issuer NAV estimations, and a DEX-derived feed - all have failure modes.

Liquidation path. When a borrower defaults, can the collateral actually be liquidated within the protocol’s liquidation window. For tokenised credit with weekly or monthly redemption windows, the on-chain liquidation path needs an explicit answer: atomic redemption, RFQ settlement, or a market maker standing behind a quote.

Governance. Who issues the collateral, who prices it, who lends against it. If the same entity holds all three roles, the credit decision and the pricing decision can lead to the conflict of interst.

Liquidity crunch. How liquid is the credit market underlying the token? Can the tokens be redeemed anytime?

The above checklist is a standard evaluation that any credit committee would apply to a structured-credit warehouse. The RWA category lacks a shared standard, so the same questions get re-asked in every integration.

What an LP should still keep in mind

The v-wmtUSDC collateral inside Select is worth a closer look, because it is structurally novel.

The collateral. v-wmtUSDC is a non-collateralised lending position to Wintermute vault issued on the Wildcat protocol. Lenders deposit USDC; Wintermute borrows against an unsecured position; yield accrues each block at a fixed APR (currently 9.25%).

The honest summary: this is fundamentally a credit decision on Wintermute, framed inside a DeFi-curated wrapper. For an LP who underwrites Wintermute as a credit, the Select vault is a reasonable way to access ~6% net yield with a transparent risk story. For an LP who cannot underwrite Wintermute as a credit, the yield premium is not free; it is the compensation for taking that credit.

If you trust Wintermute, the Select vault is one of the more honestly designed RWA-curator products on Morpho today. If you do not, or if you are an allocator who is required to apply standard separation-of-roles controls, the structural concentration is real and should be priced into how much exposure you size to it.

Closing

The Wintermute Armitage launch is one of the clearest examples to date of where curator-led RWA integration is heading. The structural questions raised here, bespoke oracles, immutable parameters as a substitute for governance, role concentration mitigated by reputation, are the questions every issuer-curator pair will have to answer over the next twelve months.

If you are an issuer, curator, or allocator working through the same trade-offs, this is the layer I work on. I help treasury allocators evaluate vault integrations from the demand side, and I help RWA issuers design curator-ready integrations from the supply side, oracle setup, separation of roles, permissioned secondary architecture, and the risk framework that supports them. Happy to discuss any of the above in more detail.